Get This Report on Hsmb Advisory Llc

Table of ContentsHow Hsmb Advisory Llc can Save You Time, Stress, and Money.The Best Strategy To Use For Hsmb Advisory LlcFacts About Hsmb Advisory Llc UncoveredThe Ultimate Guide To Hsmb Advisory LlcUnknown Facts About Hsmb Advisory Llc

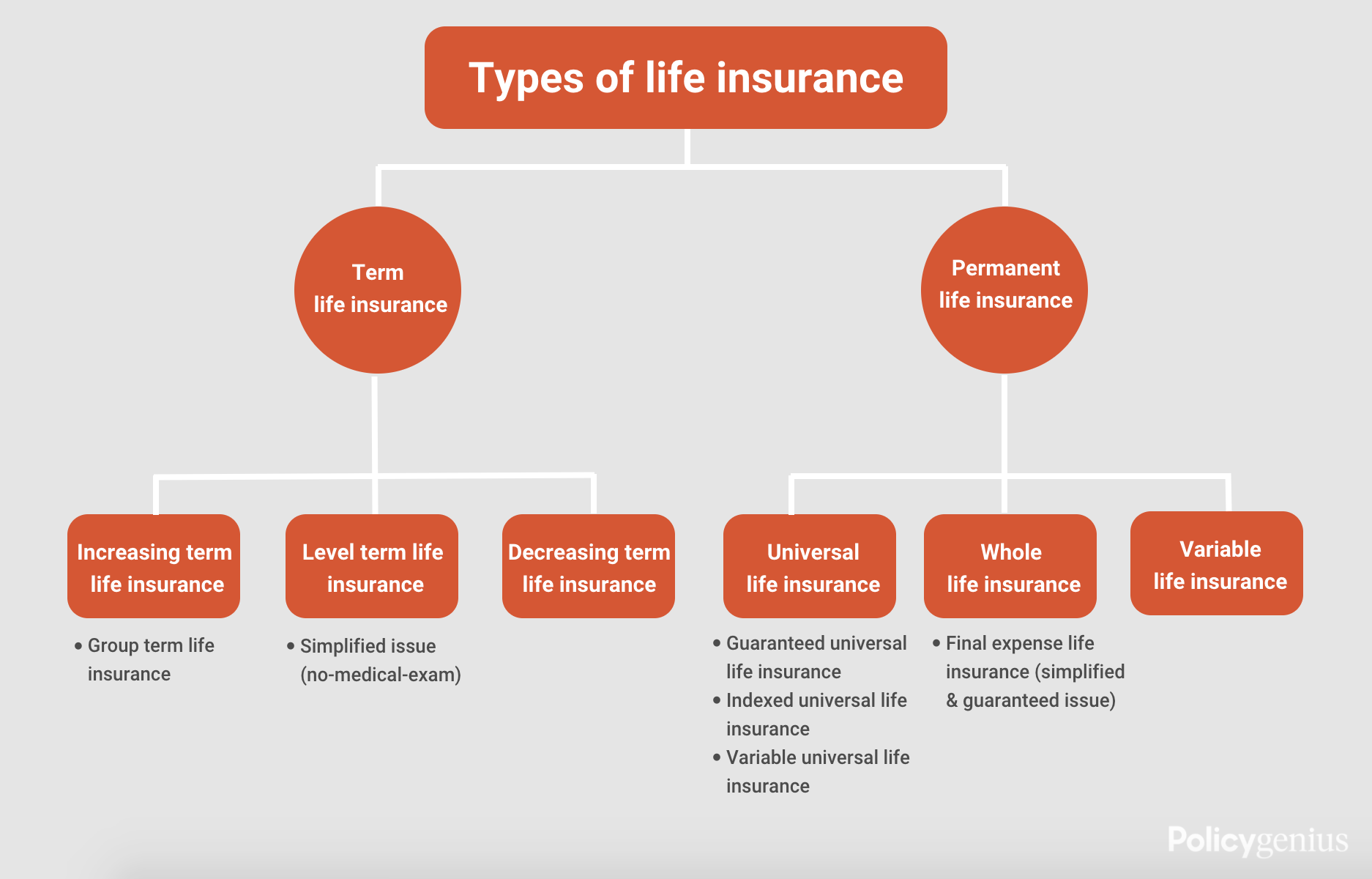

A variant, called indexed universal life insurance policy, provides a policyholder the choice to separate cash value totals up to a dealt with account (low-risk investments that will not be affected by the stock exchange) or an equity indexed account, such as Nasdaq 100 or the S & P 500. https://canvas.instructure.com/eportfolios/2754178/Home/Health_Insurance_St_Petersburg_FL_Tailored_Solutions. The insurance policy holder has the option of exactly how much to allot to every account

These are normally made use of in estate planning so there is sufficient cash to pay inheritance tax and other expenditures after the death of both spouses. Allow's state John and Mary took out a joint second-to-die plan. If just one of them is dead, the policy is still energetic and doesn't pay out.

The Single Strategy To Use For Hsmb Advisory Llc

This guarantees your lending institution is paid the equilibrium of your mortgage if you die. Reliant life insurance policy is protection that is given if a spouse or dependent child passes away. This type of protection is generally used to off-set costs that occur after death, so the amount is commonly tiny.

The Buzz on Hsmb Advisory Llc

This kind of insurance coverage is additionally called funeral insurance policy. While it might appear strange to take out life insurance coverage for this kind of activity, funeralseven basic onescan have a price tag of numerous thousand dollars by the time all costs are factored in. That's a whole lot to find out. Figuring out that you require life insurance policy is the first action.

We're here to aid you appear the mess and discover even more regarding the most popular type of life insurance, so you can determine what's ideal for you.

This web page offers a glossary of insurance coverage terms and definitions that are commonly utilized in the insurance service. New terms will be added to the glossary over time. These definitions stand for a common or basic usage of the term.

How Hsmb Advisory Llc can Save You Time, Stress, and Money.

- unforeseen injury to an individual. - an insurance contract that pays a mentioned advantage in case of death and/or dismemberment brought on by crash or defined sort of accidents. - time period insured should incur qualified medical expenses a minimum of equivalent to the deductible amount in order to develop an advantage duration under a significant clinical expense or thorough medical expense plan.

- insurance provider assets which can be valued and consisted of on the balance sheet to determine economic practicality of the business. - an insurance firm accredited to do service in a state(s), domiciled in an alternative state or nation. - occur when a policy has been processed, and the costs has actually been paid before the reliable date.

- the social phenomenon whereby individuals with a higher than typical possibility of loss seek greater insurance coverage than those with much less threat. - a team supported by participant business whose function is to gather loss statistics and release trended loss expenses. - a person or entity that straight, or indirectly, with one or even more various other individuals or entities, controls, is controlled by or is under typical control with the insurance firm.

The 20-Second Trick For Hsmb Advisory Llc

- the maximum dollar amount or total amount of insurance coverage payable for a solitary loss, or multiple losses, during a plan duration, or on a solitary job. - approach of repayment of a health and wellness strategy with a business entity that directly supplies care, where (1) the health insurance plan is contractually called for to pay the total operating expense of the business entity, less any income to the entity from various other customers of solutions, and (2) there are common endless warranties of solvency in between the entity and the health insurance plan that placed their particular resources and surplus in danger in ensuring each other.

- a price quote of the claims negotiation related to a specific insurance claim or claims. - an insurance coverage business created according to the legislations of a foreign country. The business must adapt state regulative standards to lawfully market insurance products because state. - coverages which are usually created with building insurance, e.- an annual report required to be filed with each state in which an insurer operates. https://hsmbadvisory.jimdosite.com/. This report gives a photo of the economic problem of a business and substantial events which took place throughout the coverage year. - the beneficiary of an annuity settlement, or individual during whose life and annuity is payable.